Exemptions under section 10 of the Income Tax Act | Income Tax Section 10 of the I,.T Act, 1961 described tax benefits to a salaried person. This section is displayed on income that falls under the exemption category and is not included in the total income for the year.

Therefore,

In this article, you will learn about the different items, subcategories, and exemptions of Section 10.

Basic exemptions under Section 10 of the Income Tax Act

Free Amounts Let’s take a look at each of them now.

1. Section 10(5): Tax exemption on travel grant admissible to salaried persons in India

In other words, This is an income tax exemption for individual taxpayers. Income Tax Section 10(5) of the Income Tax Act, 1961 reveals that a taxpayer can be eligible to claim a full tax exemption on the LTA component of salary. This applies to both Indian and foreign employees. The department also provides benefits to the employee’s family members, including:

• Spouse

• Children

• Country

• Siblings

You may also like- Auto Calculate Income Tax Master of Form 16 Part B for the F.Y.2022-23 & A.Y.2023-24 which can prepare at a time 50 Employees Form 16 Part B in Excel

However, in order to be exempt from tax, the following conditions must be met:

• Regarding LTA received from the employer for the employee and their dependents during the financial year

• For future employee travel (current or past)

• The exemption threshold will depend on the amount of travel taken by the eligible employee and their dependents during the tax year

• No waiver is possible unless the employee is traveling with his family

However, Let’s understand this with an example. For example, Mr. A receives an annual allowance of Rs.40,000 as part of their salary. He takes the family on two vacations. The cost of the previous flight (up and down) is Rs 21,000 comes. In the second, it reaches Rs 15 thousand. Total Rs (21,000 + 15,000) = Rs 36,000. According to this chapter Mr. B if the traveling allowance (LTA) component of their annual salary is Rs 40,000, can claim tax relief on expenses of up to Rs 36,000 during the year.

You may also like- Auto Calculate Income Tax Master of Form 16 Part A&B for the F.Y.2022-23 & A.Y.2023-24 which can prepare at a time 50 Employees Form 16 Part A&B in Excel

2. Section 10 (13A): Exemption of house rent subsidy

For instance, In India, the standard salary structure usually includes a House Rent Allowance (HRA) component, which employees can use to cover their house rent expenses. The portion of salary used for rent and accommodation is fully exempt under section 10(13A). The exemption from payroll tax will be the minimum of the following:

• Actual amount received as an employee

• 40% of salary for residents of non-metropolitan cities and 50% for residents of metropolitan cities.

• Amount paid as rent is more than 10% of the basic salary

Above all, Let us now consider an example. Nila pays a monthly rent of Rs 10,000 for her studio in Bangalore, India. He earns 12,000 and his basic salary is 20,000. Therefore, your layoffs will be minimal:

•, Rs 12,000

•, 40% (Bangalore is not a metropolitan city) ie 8000.

• Rs (10,000-10% of Rs 20,000) = Rs (10,000-2,000) i.e. Rs 8,000

Therefore, even though Nila pays a monthly rent of Rs 10,000, she can claim a tax deduction of Rs 8,000 on the HRA component of her salary.

You may also like- Auto Calculate Income Tax Master of Form 16 Part B for the F.Y.2022-23 & A.Y.2023-24 which can prepare at a time 100 Employees Form 16 Part B in Excel

3. Section 10(14): Exemption from special allowance received as part of salary

In addition, An employer can offer certain benefits to their employees as part of their salary. Although there is no upper limit to the amount an employer can designate as a special allowance, the employee must use the special allowance only for specific purposes. After that, Section 10(14) provides that special allowance shall not be taken into account in computing the tax liability of the employee for the year. In addition, special allowances are divided into two broad categories as follows:

Section 10(14)(i):

1. Every day

Employees receive this subsidy to cover their daily expenses when they are not at work.

2. Travel allowance

This type of allowance is paid to the employee for expenses incurred during official visits.

3. Single Allowance

If you are associated with a company that requires you to wear a uniform during work, the cost of obtaining or maintaining it is covered by this subsidy.

In addition,

4. Auxiliary Allowance

Similarly, It is provided to employees who need help or assistance to perform their official duties. There is a deduction under section 10 of the IT Act for wages paid to an assistant.

However

5. Transport subsidy

It helps to cover transportation expenses while traveling on official business.

6. Research or academic scholarship

It is primarily given to encourage training, research, and other academic activities.

Section 10(14)(ii)

In other words, You are responsible for paying the fee

Set for these special allowances only if they exceed the specified limit. Below are some of the benefits covered in this section and their respective limits:

1. Child Education Subsidy

Therefore, A special allowance of Rs 100 is given for the education of an employee’s child. However, your allowance is limited to 2 children per employee. This subsidy is fully exempt from tax under Section 10 of the I-T Act, 1961.

2. Subsidy is given for the highly active area

In conclusion,

The armed forces may provide such subsidies to their members under certain conditions. The tax-free threshold is set at Rs 4200 per month.

Above all,

Download Automated Income TaxPreparation Excel-Based Software All in One for the Non-Government (Private)Employees for the F.Y.2023-24 and A.Y.2024-25

Feature of this Excel Utility:-

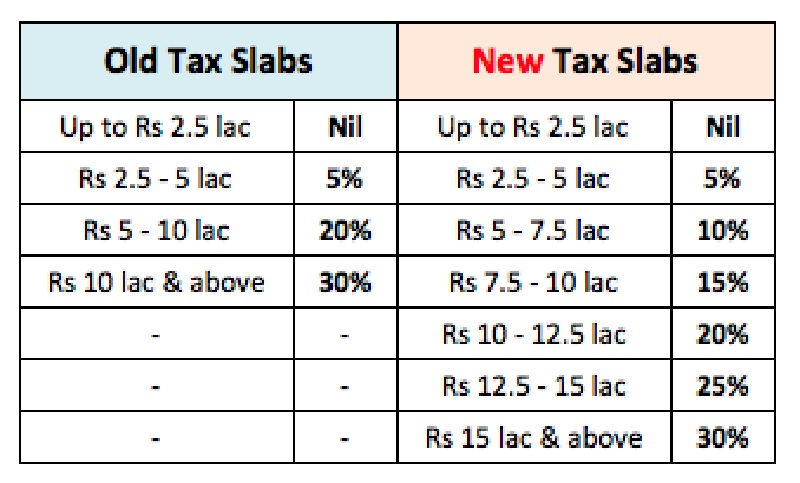

1) This Excel utility prepares and calculates your income tax as per the New Section 115 BAC (New and Old Tax Regime)

2) This Excel Utility has an option where you can choose your option as a New or Old Tax Regime

3) This Excel Utility has a unique Salary Structure for Government and Non-Government Employees Salary Structure.

4) Automated Income Tax Form 12 BA

5) Automated Income Tax Revised Form 16 Part A&B for the F.Y.2023-24

6) Automated Income Tax Revised Form 16 Part B for the F.Y.2023-24